Strategies for Navigating Elevated Interest Rates

Strategies for Navigating Elevated Interest Rates

Strengthening AR Performance in a Changing Financial Landscape

There has always been a strong correlation between the cost of funds and accounts receivable (AR) management. As interest rates increase, the cost of borrowing money also increases for businesses. Any delays in receiving payments from customers can, therefore, have a more pronounced effect on a company's bottom line profits. The impact of slow payments on profits becomes more significant because of the heightened cost of financing, increased opportunity cost of funds, cash flow constraints, disruption to working capital management, and potential reduction in profit margins.

Before Covid, we enjoyed a decade of low interest rates in conjunction with a benign economy. In such a time of easy money, receivables management becomes less critical and credit policies tend toward laxity. Now that interest rates are higher, it is time for companies to reset their credit policies in order to adjust to the current interest rate environment.

Where Are Interest Rates Headed?

For those predicting that interest rates would soon return to pre-Covid levels, the past month or so, and last week in particular, have let the air out of that bag. Expectations that the Federal Reserve will shortly start cutting rates have been dashed:

The Atlanta Fed President, Raphael Bostic, announced he expects just one rate cut in the fourth quarter.

Dallas Fed President Lorie Logan added, “It’s much too soon to think about cutting interest rates.”

Federal Reserve Bank of Minneapolis President Neel Kashkari penciled in two rate cuts for later in 2024 at the last Fed meeting but noted, "If we continue to see inflation moving sideways, then that would make me question whether we need to do those rate cuts at all."

The bond experts at PIMCO are betting that the Fed will deliver fewer rate cuts than other key central banks over the next year or two.

Friday’s strong jobs report suggests the economy is stronger than expected acting as a counterweight against rate cuts, though wage growth moderated slightly.

The issue at hand is that despite the Fed’s rate increases in 2022 and 2023, the US economy has proven to be very resilient. Faced with that reality, it is likely that at least moderate interest rates are here to stay awhile and there is no going back to an easy cash scenario for the foreseeable future. Consequently, business credit grantors need to adjust their game plan to improve their cash conversion cycle and overall AR performance in order to prevent profit dilution.

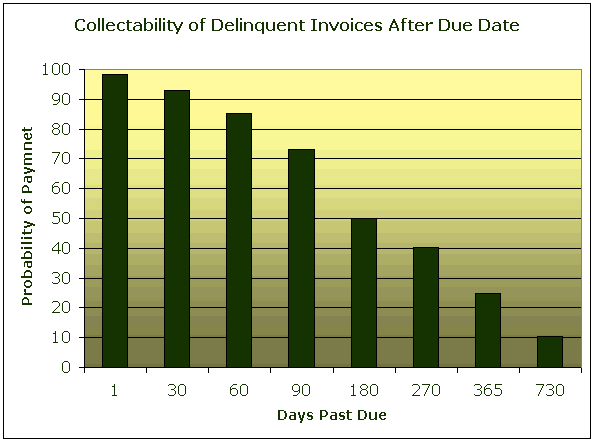

In a lower interest rate environment, the decline in collectability as shown on the above chart would be more modest for the first 90 days past due before beginning to accelerate. With elevated interest rates, however, the immediate impact can be significant. At just 60 days past due, an invoice has already lost 15 percent of its value.

To continue reading and learn ten ways to protect your company from rising interest rates — the first nine are directly related to receivables management — you need to be a paid subscriber to Your Virtual Credit Manager.

Do you need help with Portfolio Monitoring and Analysis or are there Past-Due Accounts you are trying to collect? The experts at Your Virtual Credit Manager are currently offering 33 percent off our standard consulting rates.

Readers of Your Virtual Credit Manager can access sharply discounted business credit reports from D&B, Experian, or Equifax through our partner accredit.

Please feel free to share this newsletter with your small business customers . . . it just might help them pay you sooner.

Nine Tips for Safeguarding Your AR from Interest Rates

In the face of persistent interest rates, there are a number of steps business credit grantors should take to protect the value of their accounts receivable. Implementing robust credit policies, including thorough credit checks and tight credit terms, minimizes default risks. Offering early payment discounts and leveraging technology will streamline invoicing and collection processes, ultimately strengthening financial resilience against fluctuating economic conditions. Here’s nine steps you should take to safeguard your receivables:

Strengthen Credit Policies: Review and tighten credit policies to ensure that credit is not extended to accounts that are going to become chronic collection problems. Such accounts, especially if they are only purchasing modest amounts, should be asked to pay via a credit card or offered third party financing (see #6). Conduct thorough credit checks and analysis to minimize the risk of default.

Offer Early Payment Discounts: Incentivize customers to pay early by offering discounts for early payment. For example, instead of net 30 terms offer a 1 to 2 percent discount for payment within 10 days. Many companies look for discount opportunities as a way to make their AP departments a profit center, so offering early pay discounts can help improve your cash flow and reduce your financing needs.

Implement Efficient Invoicing Practices: Streamline your billing processes to ensure accurate and timely invoicing. Consider electronic invoicing systems to expedite the billing cycle and reduce the chance of errors. Delays in generating and transmitting invoices as well as invoice discrepancies (a mismatch with your customers purchase order or delivery document.) are well documented to cause payment delays.

More Closely Monitor Your Receivables Aging: Watch out for customers whose AR is getting older and promptly follow up on overdue payments. Tighten up you collection strategy if you haven’t already implemented a systematic approach to collections, including reminder notices and escalation procedures when accounts become delinquent.

Negotiate Payment Terms: Negotiate favorable payment terms with customers, such as shorter payment periods or partial upfront payments, to accelerate cash inflows. Credit terms are part of the sales equation, so take advantage of this whenever new pricing schedules are being drawn up. Payment terms can provide excellent leverage for reaching a better understanding with your customers about your payment expectations.

Provide Financing Options: Instead of offering credit terms, there are now third-party lenders who can provide your customers point-of sale financing. Your customers get the terms they desire, and you get a discounted payment, usually in just a few days. Also, explore alternative financing options, such as factoring or asset-based lending, to improve liquidity without solely relying on traditional bank loans. You might also consider locking in favorable interest rates through fixed-rate financing on your own account or by using hedging mechanisms.

Monitor Interest Rate Trends: Stay informed about interest rate trends and adjust your credit strategies accordingly. When rates are increasing, your credit policies should be less forgiving. The opposite also holds true. Failure to adjust your credit policies will result in slower payments and accumulating more risk in your AR portfolio when rates are rising. When rates fall and you fail to adjust credit policy, you will miss out on sales opportunities.

Enhance Customer Relationships: Cultivate strong relationships with customers to encourage timely payments and foster loyalty. Good communication and transparency can help address payment issues proactively. This includes training your customers to pay promptly. With new customers, this is easily done by making it clear from the start that their initial credit limit is probationary and that a failure to pay when due will result in you require cash or an upfront credit card payment for future orders. A similar approach should be taken for customers making small purchases. If they cannot pay on time, they are not worth the additional collection effort.

Invest in Technology: Leverage technology solutions, such as e-billing platforms, collection automation and auto-cash, to streamline processes, improve efficiency, and gain better insights into AR performance. Any solution that saves time and increases productivity is going to deliver significant returns on investment.

By implementing these strategies, business credit grantors can mitigate the impact of high or rising interest rates on their cash conversion cycle and accounts receivable performance, ultimately strengthening their financial position and operational resilience.

Another Thing You Can Do . . .

While the focus of this newsletter is credit control and receivables management, elevated interest rates also affect other aspects of your cash flow and working capital requirements. Commensurate with your AR management efforts, you will want to optimize your inventory management. Efficient inventory management practices can reduce your need for financing and minimize the carrying costs associated with excess inventory.

Moving toward a lean inventory position may necessitate extending additional credit, but that can always be done by focusing your sales efforts on your better-paying customers. Once your inventory is at an optimal level, you then have more leverage to focus your sales efforts on your most profitable and best-paying customers, thereby ensuring optimal results.

It starts with businesses recalibrating their credit policies and accounts receivable management strategies to navigate the complexities of an environment marked by higher interest rates. With the prolonged resilience of the U.S. economy and indications of a sustained interest rate trajectory, the imperative to safeguard against profit dilution is more pronounced. As the landscape continues to shift, proactive adaptation remains paramount for sustaining profitability and mitigating risks associated with fluctuating interest rates.