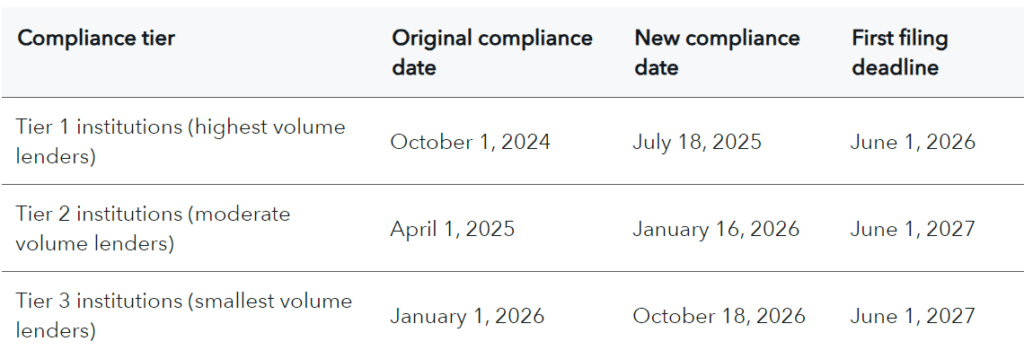

Each reporting tier and its associated deadline is determined by the number of covered transactions to small businesses that a lender originated in both 2022 and 2023.

In fact, a company or organization must have originated at least 100 covered credit transactions in 2022 and 100 in 2023 to fall under the rule’s requirements at all (i.e., be considered a “covered financial institution”) once the rule is effective.

What is a covered transaction? The CFPB generally describes it as a request for any of the following:

- Loans

- Lines of credit

- Credit cards

- Merchant cash advances

- Credit products used for agricultural purposes

Requests for additional credit on an existing loan are not counted as originations for the purpose of determining a covered financial institution.

What is an application?

For data collection and reporting, financial institutions must track applications they receive for covered transactions, as opposed to solely tracking originations. What is an application under the CFPB 1071 rule? It is an oral or written request for a covered credit transaction that is made following the procedures used by a financial institution for the type of credit requested. This means that lenders must track data not only related to approved and booked credit but also applications that are any of the following:

- Withdrawn

- Incomplete

- Denied

- Approved by the lender but not accepted by the applicant

A re-evaluation, extension, or renewal request on an existing business account is excluded from the definition of covered applications as long as the request seeks no additional credit. Inquiries and prequalification requests are also excluded.

How a lender defines an application as incomplete or withdrawn can vary from financial institution to institution, noted Abrigo Senior Advisor Paula King, CPA, who is already working with financial institutions to plan for and prepare 1071 reporting.

The CFPB “has left it up to financial institutions as to where you feel the cutoff is for an incomplete application” or a withdrawn application, she said. Regardless of how the bank or credit union defines these application resolutions, the lender should spell it out in the loan policy, King added. Loan policies should also clarify how a counteroffer by the lender will be treated.

Transactions excluded from 1071

Several types of transactions are excluded from the CFPB’s requirements to report on applications. Among those considered excluded transactions:

- Letters of credit

- Trade credit (i.e., financing arrangements such as accounts receivable with a business providing goods or services)

- Public utilities credit

- Securities credit

- Incidental credit defined in Regulation B as exempt (e.g., not payable in more than four installments; not subject to finance charge)

- Factoring

- Leases

- Consumer-designated credit used for business/ag purposes, such as taking out a home equity line of credit or charging business expenses on their personal credit cards

- Purchases of originated covered credit transactions

- Applications with potential HMDA and section 1071 overlap: CFPB does not require reporting under section 1071 (transactions would only be reportable under HMDA)

A final component of the rule that is useful in understanding the various deadlines for 1071 reporting is the CFPB’s description of what constitutes a small business. An applicant or borrower is considered a small business if it is a business (including agricultural) that had $5 million or less in gross annual revenue for its preceding fiscal year before applying.