Gleaning Actionable Insights from Credit Scores

Gleaning Actionable Insights from Credit Scores

Ranking the Customers in Your AR Portfolio Provides Greater Value Than Just Using Scores to Assess an Individual Company's Credit Worthiness

Commercial credit scores predict the likelihood of a business fulfilling its financial obligations, particularly regarding debt repayment and trade credit. As such, they are just one of the many tools, such as credit reports, supplier and bank references, and financial statement analysis, that can help assess a business's creditworthiness. Their greatest value, however, may be not what they can tell you about an individual company, but what they can tell you about your entire accounts receivable (AR) portfolio.

First, a little background. Commercial credit scores are often not as well understood as consumer credit scores such as FICO. The FICO score is an accepted standard that applies equally well to most of the consumer population. It has no commercial corollary because, unlike the homogeneity of consumer populations, businesses are an extremely diverse lot. There is little similarity, for example, between a five-employee HVAC firm and a local restaurant chain. Due to this factor, as well as smaller sample sizes, commercial credit scores will have higher variances than consumer scores.

In addition, there isn’t much uniformity from one commercial credit score to the next, and they are designed to predict a range of events. One score may indicate the chance of a company going bankrupt within the next two years while another provides the probability of going 90 days past due in the next 12 months. Still others may be predictive of default, financial distress or financial health, and creditworthiness. As a rule of thumb, however, the more specific the outcome being predicted, the more accurate will be the score. For instance, bankruptcy within the next two years is more easily defined than the more nebulous state of financial distress.

Despite these shortcomings, commercial credit scores can be valuable tools for a company offering trade credit to other businesses. Scores provide valuable insights into the creditworthiness of business customers and help companies make informed decisions regarding trade credit extension, terms, and risk management strategies. Here are the four primary ways credit scores are used:

Risk Assessment: Credit scores provide an objective measure of a business's creditworthiness based on its financial history and payment behavior. Businesses with higher scores are generally considered a lower risk, while those with lower scores pose a higher risk.

Setting Credit Terms: Scores help the person doing the analysis determine appropriate credit terms, such as credit limits and payment terms. Companies tend to offer more favorable terms to customers with higher credit scores, such as higher credit limits or longer payment terms while imposing stricter terms on higher-risk customers with lower scores.

Monitoring Credit Risk: Companies may use credit scores to monitor the credit risk of their existing customers. By regularly updating customer credit scores, businesses can identify changes in credit risk and take appropriate actions, such as adjusting credit terms or initiating collection efforts, to mitigate potential losses.

AR Portfolio Analysis: Credit scores provide the most effective way to identify concentrations of risk within your AR portfolio as well as identify opportunities to assume more risk to increase sales and profits. This is done by ranking your customers by their credit scores and then analyzing the various segments of your AR portfolio.

Of these four ways to utilize commercial credit scores, AR Portfolio Analysis provides greater returns than the other three. The intelligence gleaned will identify both risks to be mitigated and opportunities to be exploited.

To continue reading and learn the value of using commercial credit scores to rank the customers in your AR portfolio, as well as six ways to leverage customer rankings, you need to be a paid subscriber to Your Virtual Credit Manager.

Do you need help with Portfolio Monitoring and Analysis or are there Past-Due Accounts you are trying to collect? The experts at Your Virtual Credit Manager are currently offering 33 percent off our standard consulting rates.

Readers of Your Virtual Credit Manager can access sharply discounted business credit reports from D&B, Experian, or Equifax through our partner accredit.

Please feel free to share this newsletter with your small business customers . . . it just might help them pay you sooner.

The Value of Ranking Your Customers

Too often we see organizations buying credit scores but never using the scores to rank their own customers. They instead rely on the credit bureau’s calibration of high, medium, and low risk. The problem with doing that is the aforementioned variances between different industries, which can be exacerbated even more within a company’s customer portfolio. For this reason, unless you rank your own customers, you will not be able to derive full value from a commercial credit score.

This brings up another issue we see — a lack of trust in commercial credit scores. The reason for this appears to also be a result of the variance issue. Business credit executives are often more comfortable making decisions based on their own credit evaluation skills than by relying on a credit score. Anecdotally, they can identify situations where the scores were wrong, but their instincts were right. These instances occur because of the diversity inherent in any business sample. While credit scores will not always predict the expected result, they are statistically correlated to predict a much higher occurrence of a given outcome (e.g., delinquency or default) than will be found in a random sample.

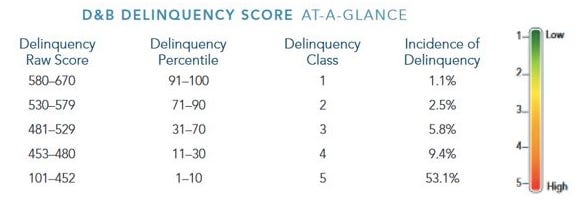

Keeping in mind that a generic credit bureau score is based upon a large universe of businesses and your customers represent a relatively tiny sample, unless you rank your customers and compare the distribution of that ranking to the distribution of the bureau score you are using, you cannot appreciate the full value of the score. The following distribution table is an example of what you should expect with a bureau score. In this case, the score is predicting a business failure in the next 12 months.

After scoring your AR portfolio, you need to count how many of your accounts fall into each delinquency percentile. Your distribution of scores is likely to skew either higher or lower compared to the bureau’s distribution. That, in turn, will tell you whether your AR portfolio’s risk exposure is higher or lower than the general business population. With that knowledge, you can begin making informed decisions. For example, if your risk is higher than the norm you may want to tighten your credit policies. Conversely, if your risk level is on the low side, you may be missing opportunities to increase sales and profits.

You should also segment your AR portfolio to see how risk is distributed by things like customer purchasing volume, distribution channel, industry type, geographic region, AR aging bucket, and so forth. This will enable you to better understand where exactly risk is concentrated in your AR portfolio so you can take steps to mitigate those risks. Needless to say, all this customer and AR intelligence is unleashed when you first use a commercial credit score to rank all your customers.

Utilizing Customer Risk Rankings

Ranking an AR portfolio by credit scores is therefore crucial for optimizing your collections efforts, mitigating credit risk, maximizing cash flow, and understanding the dynamics of your receivables asset. Here's a breakdown of why ranking is so critical, and six ways rankings can be used:

1. Identifying Credit Risk Levels: By ranking your AR portfolio based on credit scores, you can identify which customers pose the highest credit risk and which ones are more likely to pay on time. Understanding where risk is concentrated within your AR is extremely valuable in providing actionable insights.

2. Prioritizing Collections Efforts: Ranking your AR portfolio allows you to prioritize your collection efforts based on credit risk levels. Customers with the highest credit risk, as indicated by lower credit scores, can be targeted for more aggressive collection activities that start sooner than the collection strategies used with lower-risk accounts. This helps maximize collection efficiency by focusing resources on the accounts where you can have the greatest impact.

3. Setting Credit Limits and Terms: Knowing a customer’s credit score and where it falls in your rankings, will inform your decisions regarding credit limits and terms for new and existing customers. Customers with higher credit scores relative to your current AR portfolio may be granted higher credit limits and more favorable payment terms in line with their financial capacity, while those with lower scores should be subject to stricter limits and terms to mitigate risk.

4. Optimizing Cash Flow: By assigning more aggressive collection strategies to higher-risk accounts, you can improve cash flow by reducing the average days sales outstanding (DSO) and accelerating the collection of outstanding receivables. This ensures that cash is available for ongoing operations and investments, reducing reliance on external financing.

5. Mitigating Bad Debt Losses: Prioritizing collections based on credit scores will help you minimize bad debt losses by proactively addressing those customers who will tend to become delinquent before they escalate into defaults. By identifying and resolving high-risk collection issues early, businesses can reduce write-offs and preserve profitability.

6. Informing Credit Policy Decisions: Ranking the AR portfolio by credit scores provides valuable insights for refining credit policies and procedures. You can use this information to adjust credit terms, review credit approval processes, and implement risk mitigation strategies to improve overall credit risk management.

Tuning on Your High Beams . . .

Commercial credit scores serve as valuable tools for assessing credit risk, informing credit decisions, and managing relationships with business partners. They provide a standardized and objective measure of a business's creditworthiness, helping suppliers evaluate and mitigate credit risk effectively. By leveraging credit scores effectively, businesses can make informed decisions to improve overall financial performance and stability.

This is best done by first using credit scores to rank your entire AR portfolio. Once that is accomplished and compared to the credit score’s published norms, a segmentation analysis of your AR portfolio. Ranking your customers based on their credit scores will yield extremely valuable insights that otherwise would remain hidden. It’s like turning on your high beams when traveling a country road on a dark night — navigating the road ahead instantly becomes much easier.