It's Time for a Layered Approach to Collections

It's Time for a Layered Approach to Collections

Is There Any Reason to Tolerate Slow-Payments from Customers that Don't Buy Much?

The evolution of Accounts Receivables (AR) automation has revolutionized our collection strategies. Previously, decisions were largely left to the discretion of individual collectors, resulting in subjective and inconsistent approaches. Manual collection processes centered on an aged accounts receivable trial balance (ARTB) lack the regimentation and efficiency brought about by automation.

Automated collections increases productivity by providing higher visibility into all things related to a customers AR (invoices, shipping documents, previous collection efforts, and so forth), thereby saving time and driving better decisions. Collection software also provides automated workflow based on a collection strategy being assigned to each customer. The result is far more effective and efficient collection effort compared to collections based on manual processes.

Please feel free to share this newsletter with your small business customers . . . it just might help them pay you sooner!

The collection theory derived from automating the process is also relevant to organizations that still handle collections manually. First, collection software greatly reduces the time spent on preparing to make a collection call or sending a dunning notice as well as the time spent on follow up activities post-contact with the customer. This provides more time for customer contacts. Secondly, prioritizing collection efforts and following a graduated sequence of collection activities (a collection strategy) with each past due account is much more effective than ad hoc collection efforts guided by the collecting working through an aged trial balance. Creating more time for collection activities and being more strategic with the sequencing of those activities will also provide substantial cash flow benefits to organizations that rely on manual collection processes. For a more in depth discussion of systematic collections, click here.

The experts at Your Virtual Credit Manager are ready to help you improve cash flow and reduce AR risks during these challenging times. What do you need help with? We are currently offering 33 percent off our standard small business consulting rates.

The Traditional Approach to Automating Collections

Automation introduced a structured approach to collection strategies, driven by trigger events such as days past due, missed payments, or non-responsiveness to communication. Distinctions are made based on the amount past due and the risk associated with each customer. Larger balances and higher-risk customers receive more personalized and persistent collection efforts, while accounts with smaller balances and lower-risk are addressed through a heavier dose of automated dunning notices.

Table #1: Traditional Collection Automation Strategies

This automated approach, as illustrated in Table 1, significantly reduces Days Sales Outstanding (DSO), typically resulting in a 10 to 20 percent reduction within six months for newly automated collection organizations. However, that doesn’t exclude an opportunity to do even better.

Read on to learn how a better understanding of the revenue distribution within your customer portfolio can facilitate a more layered approach to the assignment of customer specific collection strategies that will help you control costs and improve cashflow.

Why You Need to Consider Revenue Distribution

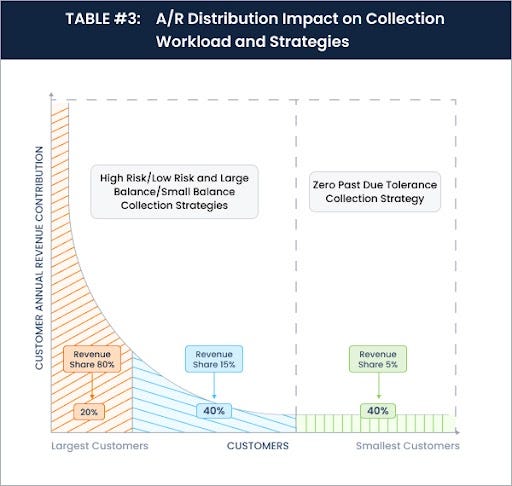

Despite the success of automated collection strategies, there's a need to reconsider the distribution of revenue generated by the accounts receivable portfolio. Pareto's Theorem (the 80/20 rule) reveals that a significant portion of revenue comes from a limited number of customers. To optimize collection resources, I recommend dividing the AR portfolio into three segments based on revenue contribution:

Top 20 Percent: Customers contributing to 80 percent of revenue.

Next 40 Percent: Customers contributing approximately 15 percent of revenue.

Bottom 40 percent: Customers contributing only about 5 percent of revenue.

Implementing a zero-tolerance collection policy for the smallest account segment (see Table #2) allows for a more streamlined and automated approach, reducing the collector's effort. If you don’t have collection software, a series of email templates will still prove to be an efficient dunning tool. This strategy aims to train smaller accounts to pay on time, with failure to do so resulting in a shift to payment being required at the point of sale.

The expected results of this zero-tolerance strategy include:

A decrease in the number of small customers on open terms

Substantial decline in small-dollar past due receivables

A reduction in collection efforts for the least cash-flow-generating customer segment

Increased attention to the larger customers that contribute most of your revenue

Readers of Your Virtual Credit Manager can access sharply discounted business credit reports from D&B, Experian, or Equifax through our partner accredit.

Over time, insights gained from this approach can inform risk assessments for new accounts, which you can use to refine your credit risk parameters. Embracing a zero-tolerance policy doesn't necessarily mean turning away sales, especially considering there are now other payment options such as credit cards and Buy-Now-Pay-Later (BNPL) solutions in the B2B payment ecosystem. Instead, you should be encouraging new accounts to utilize these alternative channels rather than applying for open credit terms. Along these lines, you should also consider setting an order threshold under which you do not offer open credit terms.

Further Applications and Continuous Improvement

To maximize the benefits of this zero-tolerance collection strategy, consider:

Further tailoring your collection strategies for consistent but slow-paying, lower-risk, larger-dollar accounts — since the risk of non-payment is minimal a collection strategy with a soft initial reminder followed by more aggressive efforts if they don’t pay as per usual will be more efficient than the traditional approach

Shifting the time saved in dealing with the zero-tolerance segment towards more aggressive strategies for high-risk accounts

Gradually extending the zero-tolerance approach to a larger segment of customers, based on the performance results realized

Embracing automation is not just a one-time change but an ongoing process of refinement and optimization. Regularly revisiting and adapting collection strategies based on insights gained is crucial, even if you haven’t automated AR. If you haven't revised your strategies significantly in the past year, there's likely ample room for improvement in collection efficiency and effectiveness. That directly translates into better cashflow.