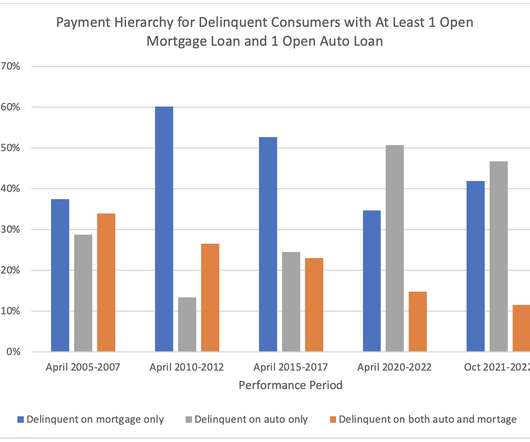

Consumers Prioritize Mortgage Payments Over Auto

FICO Blog

FEBRUARY 10, 2023

We studied this on three pre-pandemic performance periods (pre-Great Recession 2005-2007, post-Great Recession 2010-2012, and pre-pandemic 2015-2017) as well as two pandemic-era periods (2020-2022 and a one-year period from 2021-2022).

Let's personalize your content